“Productive Conversations”

Why the most expensive words in markets are the ones everyone already believes

“In time, those Unconscionable Maps no longer satisfied, and the Cartographers Guild struck a Map of the Empire whose size was that of the Empire, and which coincided point for point with it.”

- Jorge Luis Borges, “On Exactitude in Science”

On a Friday afternoon in March, Donald Trump told reporters that the United States had been having “productive conversations” with Iran. Markets surged. Oil fell. The relief was instant and reflexive.

Marvin Barth, a former Barclays macro strategist who now runs a research outfit called Thematic Markets, saw the phrase and felt his stomach drop — not because of what it meant, but because of what it always means.

“Productive conversations” is the exact phrase Trump uses every single time he’s stalling for time. The same words. The same cadence. The same effect on markets. And every time, it means nothing.

Within hours, Iran fired missiles at the US military base on Diego Garcia — at roughly twice the range of anything Western intelligence had attributed to their arsenal. The message was not diplomatic. It was ballistic.

The map said peace. The territory said war.

"The most erroneous stories are those we think we know best — and therefore never scrutinize or question."

- Stephen Jay Gould

There’s a vocabulary of reassurance in markets and politics, a small set of phrases that mean almost nothing but move almost everything. “Productive conversations.” “We’re monitoring the situation.” “Markets are functioning normally.” “Talks are progressing.” Once you learn to hear them, you can’t unhear them. They are the sound of someone who needs you to hold still while the ground shifts beneath your feet.

At 49, I have heard all of these far too many times.

In the summer of 2008, I sat in front of a screen on the Goldman trading floor in 1 NY Plaza, watching a trade I believed in completely come apart. The thesis was sound. The data was clean. Three separate research houses agreed with the positioning. By the third morning, I was down more than I’d made in the previous four months. I remember staring at a cup of coffee that had gone cold two hours earlier and thinking: everything about this is right except what’s happening to my P&L.

The world the thesis described had moved on sometime in the previous three weeks, and I’d been too busy admiring the map to notice.

"It is difficult to get a man to understand something when his salary depends on his not understanding it."

- Upton Sinclair

I’ve been thinking about that lesson every day for the past month. Because the gap between the maps we’re being handed right now by markets, by governments, by the information machinery that surrounds us and the territory underneath has never been wider.

Let me show you what I mean with a number.

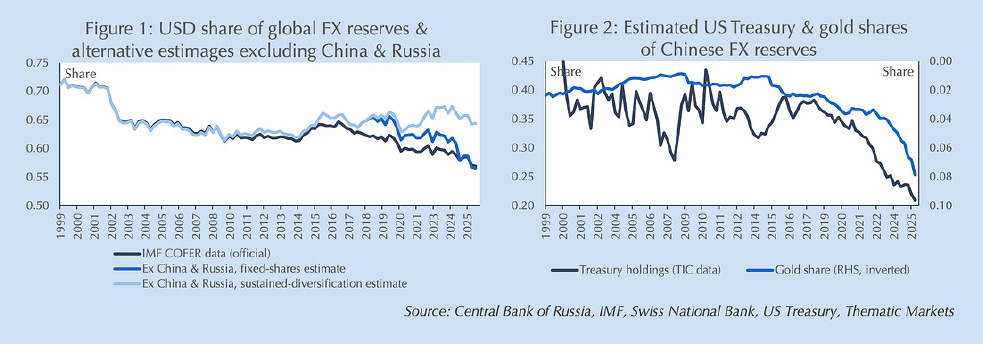

The dominant market narrative of the past two years has been de-dollarisation. Central banks are dumping the dollar. The reserve currency is in decline. Gold is the escape hatch. You’ve read this story a hundred times. It launched a thousand portfolio reallocations and pushed gold to one of the most extreme overvaluations in its recorded history.

Barth went and checked.

He decomposed the IMF’s reserve data, extracted Chinese and Russian holdings through a forensic accounting reconstruction, and found something that made me wonder why no one had looked at this before:

Every country on earth except Russia and China increased their dollar holdings over this period.

Every single one.

The entire decline in the dollar’s share of global reserves, the entire narrative, was two countries pulling out of the US financial system for geopolitical reasons. Not a loss of faith. Not debasement. A divorce. A different story entirely.

And gold?

The last time someone bought at a comparable overvaluation was January 1980.

They didn’t see that price again for thirty years.

That’s the distance between the map and the territory on the single most crowded trade in global macro right now.

You might wonder how the gap gets this wide. How millions of intelligent, well-resourced people end up trading a story that the data doesn’t support.

The short answer is that the production of maps has been industrialised.

Start with politics. In 1988, a political scientist named Murray Edelman made an observation so simple it’s almost rude: the political world that citizens encounter through news and public discourse is not a distortion of reality. It is reality. For most people, there is no other. Problems are constructed to justify solutions that already exist. Leaders are symbols, not agents. Enemies are manufactured to hold coalitions together.

And Edelman’s sharpest line:

The spectacle moves. The structure doesn’t.

Now add a factory.

When you pause for three seconds on an Instagram post, that pause is harvested, packaged, and sold to someone who wants to know what you’ll buy next Tuesday. When you speed up while scrolling, that acceleration is data too. In 2016, 89% of Google's parent company revenue came from selling predictions about what people would do next. Today, that share has dropped to about 75% — but only because other businesses grew alongside it. The prediction machine itself nearly quadrupled, to roughly $300 billion a year. Bets on human behaviour, at planetary scale, are not slowing down. They're compounding.

Shoshana Zuboff, who spent a decade studying this system, showed that the companies running it aren’t just watching your behaviour. They’re shaping it. The most profitable data doesn’t come from observing what you do. It comes from nudging you toward what someone else has already paid for you to do.

Your future, what you’ll want, choose, and believe, is being sold before you get to live it.

Now add the state. Jacob Siegel, a veteran who came home from Afghanistan in 2012 to find American culture reshaped by something he couldn’t name, spent a decade tracing the merger. The FBI had a dedicated Slack channel with Twitter executives. Censorship coordination ran through the Department of Homeland Security. The platforms and the government didn’t conspire in a back room. They fused, gradually, structurally, and almost invisibly.

The result is a map-manufacturing system of extraordinary power and extraordinary fragility. It can wrap the globe in a narrative almost instantaneously. And that narrative will shatter just as fast, replaced by the next one before you’ve finished processing the last.

The speed is the point. If you’re always reacting to the latest map, you never look down.

Which brings us back to the war.

On February 28, the United States and Israel began bombing Iran. Within the first week, something broke in the market’s pattern recognition. The cycle of escalation and de-escalation that algorithms had been trained on, parse a presidential statement, price a barrel, repeat, stopped working.

Barth titled his analysis Alea Iacta Est. The die is cast and discussed it with Grant Williams. His point was structural: once you commit to destroying a regime, the option to return to the status quo ante disappears. Both sides now face a world where backing down is more dangerous than pressing forward. Every incentive on the board has changed.

The map said Trump would escalate, extract a deal, and declare victory - the TACO.

The territory was different. Iran answered every pause with a provocation. Gulf states that had opposed the war before it started flipped within weeks to demanding the US finish what it started, not because they wanted war, but because a half-finished war was the worst outcome they could imagine.

Gregg Carlstrom, reporting from Riyadh for The Economist, captured the gap in a single observation: no one in the Gulf knew what America’s actual war aims were. They asked Washington. They got nothing back. They were living in the territory, missiles hitting apartment blocks in Bahrain, drones striking the US embassy down the street, while New York was trading the map.

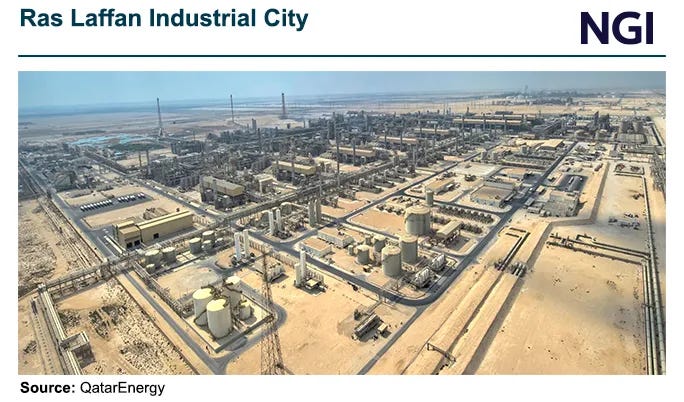

And then this fact, which we need to think about more: Three percent of global LNG supply. Offline for three to five years. From a single strike on Qatar’s Ras Laffan facility.

That will compound quietly, long after the market has moved on to the next “productive conversation.”

It is territory.

Barth draws a distinction in his work that I think is the most useful framework I’ve encountered this year.

He separates narratives from themes.

A narrative is a story that drives price but floats free of fundamentals. De-dollarisation. The debasement trade. The assumption that Trump always backs down. Narratives are powerful. They move billions. And they can persist for months or years after the facts beneath them have changed.

A theme is a structural force operating over decades. The bifurcation of the global economy along geopolitical lines. The redrawing of energy maps by war. Themes are quiet. They don’t trend. They don’t generate engagement. They just compound.

The GENIUS Act, which most people read as crypto legislation, is a piece of geopolitical statecraft designed to block China’s expansion of alternative payment rails by creating dollar-denominated stablecoin alternatives. The war in Iran, whatever its outcome, has already reshaped the global energy dependency map for a generation. These are themes. They are the territory. And almost nobody is talking about them, because the map is so loud and so fast that it drowns out everything that moves slowly and matters permanently.

I keep thinking about that Friday afternoon.

Trump says “productive conversations.” Markets move. Billions change hands. And somewhere, a handful of people hear the phrase and feel something different from relief, a quiet recognition: I’ve heard these exact words before. They mean the opposite of what everyone thinks they mean.

A few hours later, the missiles prove them right.

And it’s hard to fight that urge. I saw the same headline. I felt the same relief. For about forty-five seconds, I believed the map too.

The difference between forty-five seconds and forty-five days is the whole game. It’s the difference between catching yourself and getting caught. Between the reflex and the recognition.

I don’t know how you teach that. I don’t think you can automate it. I just know it’s the most valuable thing I’ve developed in twenty-six years of doing this, and it came entirely from the times I got it wrong.

Share this with someone who’s still reading the map.

This publication and its authors are not licensed investment professionals. Nothing produced under the Curious Mind brand should be construed as investment advice. Do your own research.

Thank you for the kind attention to my research in everyone’s weekly must read of what’s important! (Well, everyone who’s so far discovered it!)

Inspiring and insightful, thank you!