Schrödinger's Economy

AI is sending stocks to infinity and zero at the same time

What happens when the most deflationary force in history meets a system that can't survive without inflation?

I’ve been sitting with a thought for the past few weeks that I can’t resolve. And I think that’s the point.

Some of the smartest people I’ve listened to recently are making completely opposite predictions about what happens next in the economy. Both sides are airtight. Both are backed by data. And both cannot possibly be true at the same time.

Except I think they are.

We are living inside Schrödinger’s box.

The economy is heading toward an unprecedented boom and an unprecedented crisis simultaneously. The cat is alive and dead. Nobody has opened the box yet. And the strange part is that the same force, the exact same force, is driving both outcomes.

Those forces are AI & Energy. And what you believe about the next decade depends entirely on which variable you’re watching.

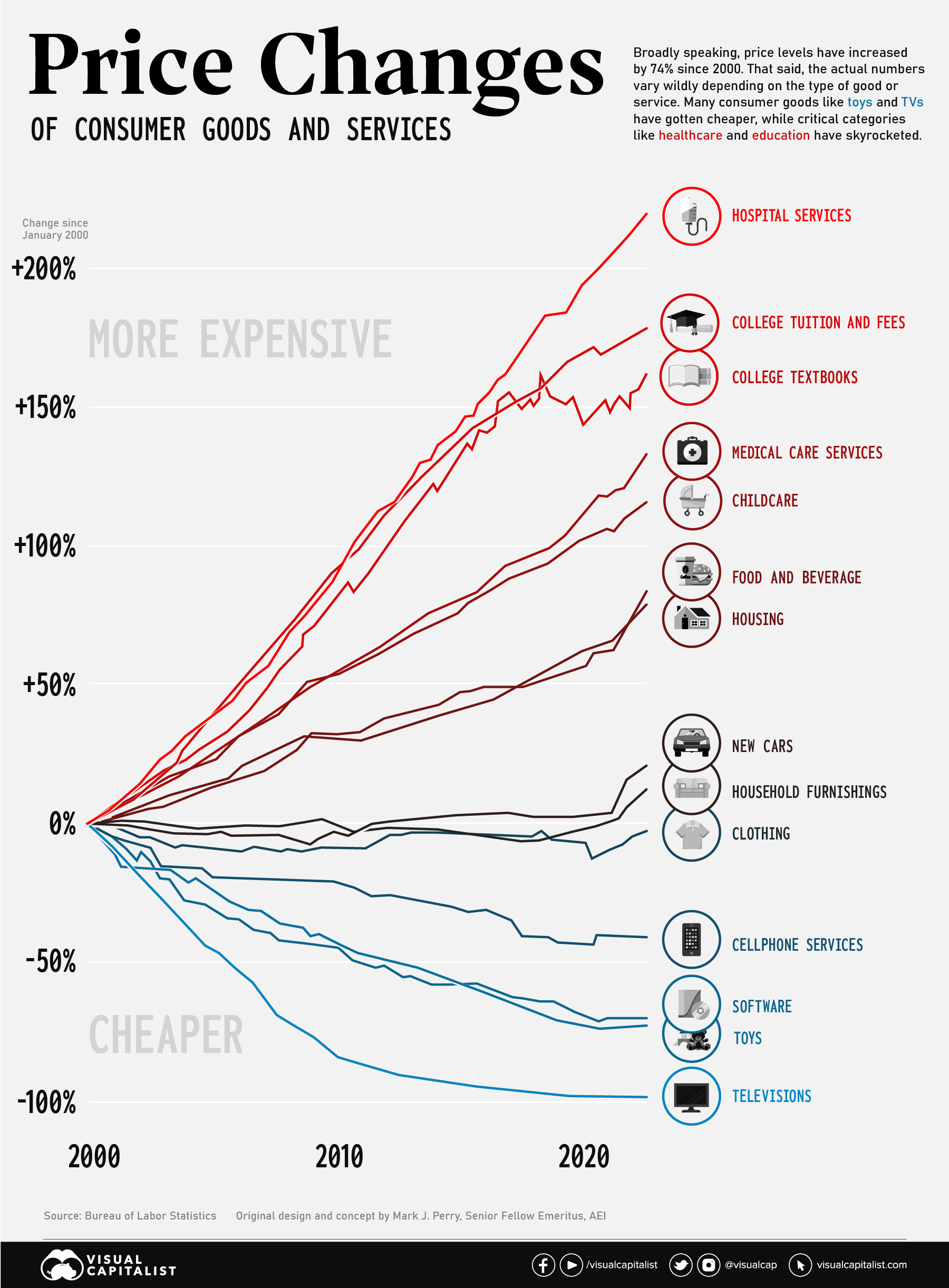

The Deflation Dividend

The logic is straightforward: AI drives productivity gains. Productivity gains push down the cost of goods and services. When things cost less, your existing income buys more. This is functionally the same as giving everyone a raise without changing a single paycheck.

We’ve already watched this movie three or four times. A television that cost $5,000 in 1990 costs $300 today and is incomprehensibly better. Communication went from dollars per minute to free. Computing power that filled a building now fits in your pocket. Each of these revolutions made nearly everyone richer in real terms, even as prices collapsed.

Andreessen’s point is that AI does this to everything else. Healthcare. Legal services. Education. Accounting. The sectors that have stubbornly resisted cost reduction for decades are exactly the ones most exposed to what’s coming. If the cost of a medical diagnosis drops by 90%, the entitlement crisis everyone worries about starts to look very different.

There’s a demographic argument too, one that doesn’t get enough attention: the world’s population growth is slowing fast. Many developed nations are already shrinking. We are going to have fewer workers. Fewer workers means less output, lower growth, a smaller pie. Unless something fills the gap. AI isn’t replacing humanity. It might be arriving just in time to prevent a slow-motion labor crisis.

Here’s the part that matters most for the skeptics: every major wave of automation in recorded history created more jobs than it destroyed. Every single one. The new roles were always ones nobody could have predicted beforehand. A software engineer in 1920 is a nonsense phrase. A social media manager in 1995 is science fiction. These jobs always seem obvious in retrospect and impossible in advance. Andreessen is betting this time is no different.

The future, in this telling, isn’t utopian or dystopian. It’s incremental. AI makes you 10% more productive this year, 15% the next. The economy adjusts. New categories of work emerge. The transition is bumpy but manageable.

If that’s the whole story, you can stop reading here and go buy the S&P 500.

It’s not the whole story.

The Speed Limit

The AI revolution runs on data centers. Data centers run on power. Not hypothetical power. Not future power. Real electrons, right now, in quantities that are genuinely hard to comprehend. The demand projections for AI compute over the next decade are creating an energy gap that no existing infrastructure plan comes close to filling.

And the bottleneck isn’t just technical. It’s political. NIMBYism is blocking new generation capacity, new transmission lines, new everything. Arnold sees geothermal as the most promising near-term solution, but “near-term” in energy infrastructure still means years, not months.

This matters because the entire bull case rests on speed of deployment. If AI is the most deflationary force in 10,000 years but it takes 25 years to fully deploy because we physically cannot power it fast enough, then the story changes. The deflation arrives slowly. Unevenly. In fits and starts.

Arnold has a trader’s instinct about this. He spent his career making decisions under genuine uncertainty, where the whole game was sizing your bets for a world you cannot predict. His read on AI infrastructure tells you something important: the physical world gets a vote. And it hasn’t voted yet.

The Slop Tax

There’s another crack in the optimistic thesis, and you can feel this one in your own inbox right now.

Cal Newport highlighted a concept recently that I haven’t stopped thinking about: work slop.

Here’s what’s actually happening inside companies that have adopted AI tools: because it costs almost nothing to generate a 10-page memo, a detailed proposal, or a lengthy email, people are generating them constantly. The output of organisations is exploding. But the quality is often terrible. And here’s the part that matters: evaluating, responding to, and sorting through all of this AI-generated material still requires human attention. Real, expensive, finite human attention.

The productivity gains in creation are being devoured by the productivity losses in consumption. You can write a report in 10 minutes that used to take two days. Wonderful. But now everyone else did the same thing, and you have 15 reports to read instead of two. The net gain in actual productivity? Far less than the brochure promised.

An economy can produce more and be worth less at the same time. That is a sentence worth sitting with.

Newport goes further. He thinks the narrative of one giant AI model getting smarter every year until it does everything is hitting a wall. Post-GPT-4, the scaling laws show diminishing returns. The future is probably hybrid, bespoke systems assembled for specific tasks, not a single omniscient machine. Which means the transition will be messier and more gradual than either camp expects.

So the bull case has real cracks. The deflation might be slower than promised, partly illusory, and bottlenecked by physics. But the truly uncomfortable question isn’t whether the bull case is wrong. It’s what happens to the financial system if it’s right.

The Debt Trap

Luke Gromen has a crucial argument about the economic system we inhabit.

The United States, like most developed economies, runs a debt-based financial system. This is not a political statement. It’s an accounting identity. The system functions, and can only function, when nominal GDP grows fast enough to service existing debt. This requires some combination of real growth and inflation. Preferably both. Always both.

Now consider what AI does to this equation.

Roughly 52% of US federal tax receipts are tied to employment. Income taxes. Payroll taxes. The jobs most immediately exposed to AI are white-collar, knowledge-economy jobs. These are, not coincidentally, the highest-paying jobs. The ones generating the most tax revenue per worker.

The math is straightforward and the implications are severe. If AI displaces even a fraction of that workforce over the next decade, federal receipts don’t stagnate. They fall. And they fall at exactly the moment when entitlement spending is accelerating due to an aging population.

So you get a doom loop. Receipts drop. The deficit balloons. The government borrows more. But the bond market is already nervous about the debt load, so borrowing costs rise. Which makes the deficit worse. Which requires more borrowing.

The usual escape valve is inflation. Print money, devalue the debt, make the nominal numbers work. Governments have done this for centuries. But here’s Gromen’s key insight: if AI is genuinely deflationary, the printing press doesn’t work as well. You’re trying to inflate your way out of a debt spiral while the most powerful deflationary force in history pushes the other direction.

This is where the Schrödinger metaphor stops being cute and starts being precise. The deflation that is wonderful for consumers is catastrophic for the sovereign debt structure. Same force. Two opposite effects. Running simultaneously in the same economy. Stocks go to infinity and zero at the same time.

Gromen sees the early warnings already. The Japanese bond market is behaving strangely. The historical relationship between gold and real interest rates has broken. He draws a parallel that should make you uncomfortable: February 2026, he says, feels like July 2007. The signals were there before the financial crisis too. Most people weren’t watching the right charts.

And at some point, Gromen argues, the US will face a choice it has been deferring for decades: save the dollar or save the economy. You can protect one. You cannot protect both. That choice, whenever it arrives, will be the moment somebody opens the box.

The Four Paths

An encoding, in Collins’ framework, is the deep structural pattern that governs how a system actually behaves. Not the surface story. The underlying logic. And the encoding underneath Schrödinger’s Economy is this: every debt-based system eventually collides with a deflationary force, and the outcome never depends on the force itself. It depends on the institutional response.

This has happened before. Not with AI, but with other technologies that dramatically reduced costs. The question was never “will this technology change everything?” The answer was always yes. The question was whether the financial and political systems adapted fast enough to absorb the shock without shattering.

Sometimes they did. Sometimes they didn’t. The encoding is the same.

So what resolves the paradox? I see four paths.

Path one: inflate anyway. Governments print money aggressively to keep the debt serviceable, choosing to sacrifice the currency rather than the economy. Asset prices soar. The cost of some things collapses while others explode. You get a deeply strange, bifurcated world where a medical diagnosis costs $5 but a house costs $3 million. This is probably the most likely outcome.

Path two: a controlled restructuring. A new financial architecture, a modern Bretton Woods, that resets the system for a deflationary world. Possible, but it would require international coordination that feels unlikely given current geopolitics.

Path three: something breaks. The bond market. A major bank. A currency. The box gets ripped open by force before anyone is ready. This is 2008 again. This is what keeps Gromen up at night.

Path four: the slow burn. AI adoption takes long enough (Arnold’s energy bottleneck, Newport’s asymptote) that the system adjusts organically. The paradox resolves through patience. This is, implicitly, what Andreessen is betting on.

Nobody knows which path we’re on. What concerns me is how few people are even asking the question. Most market participants, most policymakers, most commentators have picked a side. Boom or bust. Almost nobody is holding both possibilities in their head at the same time.

What to Build Before the Box Opens

Collins has another concept I keep returning to: productive paranoia.

The people and institutions that survive discontinuities aren’t the optimists or the pessimists. They’re the ones who build for growth while preparing for catastrophe. Not sequentially. Simultaneously.

That’s the Schrödinger’s Economy playbook. But it’s incomplete without one more idea, and it’s the one that changed how I think about all of this.

Collins talks about “return on luck.” His research suggests that most people encounter roughly the same amount of good and bad fortune over a lifetime. The difference between those who thrive and those who don’t is almost never the quality of their luck. It’s the return they get on it. Most luck, good and bad, goes completely wasted because people don’t recognize the turning point until years after it has passed.

The AI transition is luck. Enormous, world-reshaping luck arriving for all of us at the same time. Your return on it will depend on a few things.

Whether you’re already in motion. Collins calls this the 20 Mile March: disciplined, consistent effort maintained through all conditions, up markets and down, hype cycles and winters. Luck finds everyone, but it finds some people mid-stride and others standing still. You cannot capitalize on the biggest economic shift of your lifetime from a standing start. The opportunity does not wait for you to warm up.

Newport’s work lands here precisely. The ability to do deep, focused, original thinking is becoming the rarest skill in the economy. Not because people lack the capacity, but because everything in modern life is engineered to prevent it. Newport talks about cognitive strain the way a coach talks about heavy lifts: the discomfort is the point, and most people spend their entire careers avoiding it. In a world drowning in AI-generated slop, the person who can sit with a hard problem for hours and produce something genuinely new will be the last one standing. Boom or bust, that person wins. Treat your ability to concentrate the way an athlete treats their body. Train it daily. Protect it fiercely. That is your 20 Mile March. That is the thing no AI can replicate.

Whether you’re paying attention to the people around you. Collins talks about “who luck,” the idea that the most consequential form of fortune isn’t an event or a market move. It’s a person. The right mentor, partner, or collaborator appearing at the right time. But the return on who luck depends entirely on what you do next. Do you go deep with that person? Do you commit to the relationship, invest real time, follow up when it’s inconvenient? Or do you let it become another LinkedIn connection you never spoke to again? In a period of disruption, your relationships will compound faster than any asset class.

Whether you can extract value from the bad luck too. This is the part that sticks with me most. Collins doesn’t treat good and bad fortune as separate categories. In his framework, setbacks generate returns just like windfalls do. The question is whether a disaster teaches you something that compounds over the next decade, or whether you just take the hit and move on unchanged. The people with the highest return on luck are the ones who come out of their worst years with something they didn’t have before. A skill. A conviction. A scar that made them pay attention to things they’d been ignoring.

This connects to what Collins calls self-renewal: the willingness to let go of the identity that got you here in order to become the person who gets you there. Most people define themselves by their current role, their current expertise, their current position in the economy. That’s fine in stable times. In an economy that may look completely different in five years, the ability to shed an old version of yourself and build a new one isn’t a nice-to-have. It might be the whole game. The people who cling to what they were will be standing still when the luck arrives.

Financially, Gromen’s Jacob Fugger Portfolio is worth knowing: 25% gold, 25% cash, 25% blue-chip equities, 25% productive real estate. It’s not optimized for any single scenario. It’s designed to be impossible to kill. In a world where you genuinely don’t know whether deflation or inflation wins, an unkillable allocation might be worth more than a brilliant one.

But the real portfolio that matters isn’t the financial one. It’s the one you build out of deep skills, real relationships, and the willingness to move when the moment arrives. Arnold spent his career making asymmetric bets where the downside was bounded but the upside was open. That’s not just a trading philosophy. It’s a way to live through a period where nobody, and I mean nobody, knows what happens next. Invest in things where being wrong costs you little but being right changes everything. A new skill. A deeper relationship. A harder problem than the one you’re currently solving.

Schrödinger’s cat is both alive and dead. But only until someone opens the box.

Someone always opens the box. The question is what you’ve built before they do.

I've read the majority of these posts, and I am here to say that this is my favorite. I have never experienced so much cognitive dissonance in 15 minutes in my lifetime:). Lots of competing narratives here, and I honestly can't say which ones I think will prove true.

This is great - I am observing an evolution in your writing - moving into greater depth